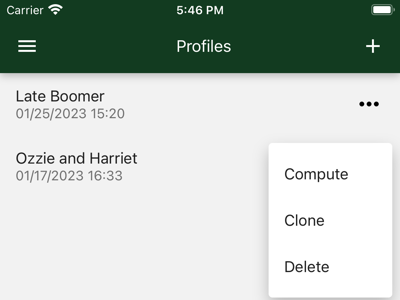

Hedgematic maintains a list of your profiles. You might create several profiles to see the effects of different choices you have.

Create your first Hedgematic profile by pressing the plus sign, proceeding to describe yourself and your retirement position:

Demographics: e.g. Birthday, age, and sex.

Social security: Estimated check? Have you started?

Expenses: After tax, after inflation spending requirements for each year of your retirement.

Balances: Your assets by account.

Once you create a profile, select the dot menu to access the following actions:

Compute a complete after-tax retirement portfolio, hedged against market risk and inflation. Can I retire today? If not, how much am I short? When do I start social security?

Clone a profile to create a new profile, based on the existing one. Stack them up against each other. There is no “edit profile” feature." This is so you can repeatedly run scenarios over time and compare the results. Instead of editing, clone an existing portfolio, enter a new name, and apply your changes.

Delete a profile, and any computed results for it.

If you just tap the profile you get a summary of that profile’s settings.

1 - For Starters

Create a personal profile to submit to Hedgmatic

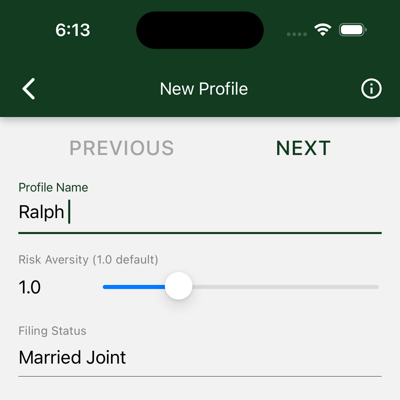

When creating a new profile, Hedgematic guides you through some initial data collection. To get started, you first provide three values.

Profile Name is displayed with the profile and any results computed from that profile. It is required and must be unique.

Risk Aversity requires some explanation. Your portfolio works like a variable annuity. For the remainder of your life, your portfolio pays you every year. The default value is 1.0. Lower numbers increase the chance that individual years may come up short. Higher values offer more security. Recommended: 1.0 is tuned to give you the maximum estimated risk-adjusted return. Lower values are more likely to risk principal; higher values approach a cash-only portfolio.

Filing Status is your IRS filing status. It is used for two purposes:

Hedgematic uses this value when computing taxes on your portfolio.

If you select ‘married’, Hedgematic will ask for information about your spouse and incorporate it in the analysis.

Buttons at the top of the page are used to navigate through these initial dialogs:

PREVIOUS takes you to the previous page (if available).

NEXT takes you to the next page (if available).

SUBMIT Seen on the last page, saves your new profile and returns to the Profiles page

You can’t click these buttons if there are any errors on the page. Fix them first.

If you click the back arrow, profile creation is cancelled and you are returned to the profile list.

2 - Your Information

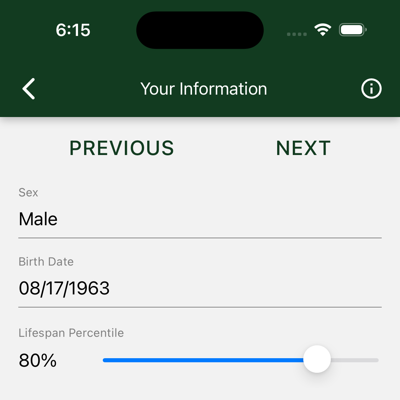

Enter some basic demographic data

Use this form to enter personal data and social security information.

Sex: Male, Female, or Unspecified. Birth Date, Sex, and Lifespan Percentile are used to calculate your lifespan and consequent Social Security payments.

Birth Date: Your date of birth.

Lifespan Percentile: A number between 1% and 99%. If you think you will outlive 75% of your High School class, enter 75.

3 - Your Spouse's Information

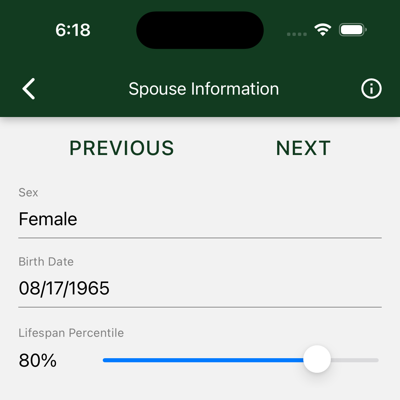

Enter some basic demographic data for your spouse

If you selected “married joint” for your tax filing status, you will be shown this form. It looks like the previous page, which can be confusing.

Use this form to enter personal data and social security information for your spouse.

Sex: Male, Female, or Unspecified. Birth Date, Sex, and Lifespan Percentile are used to calculate your lifespan and Social Security payments.

Birth Date: Your date of birth.

Lifespan Percentile: A number between 1% and 99%. If you think you will outlive 75% of your High School class, enter 75.

4 - Social Security

Social Security Information

Hedgematic incorporates your social security payments into your profile and uses them in its computations. Use this dialog to provide social security information for you and your spouse.

Social Security Terms

Social Security, and Hedgematic, use certain terms to discuss Social Security concepts:

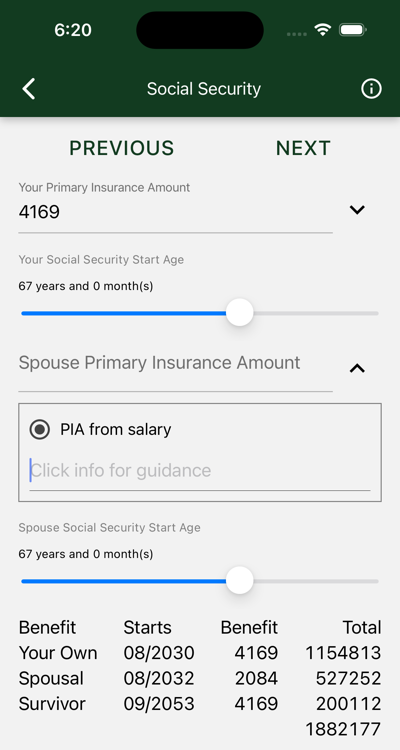

Your Start Age is the age, expressed in years and months, you start taking Social Security benefits.

Your Full Retirement Age, or FRA, is the Start Age where Social Security says you get your “full benefit”. It is determined by the year you were born.

Your Primary Insurance Amount, or PIA, is the gross benefit you get if you retire at your FRA.

Your Gross Benefit is your benefit before Medicare or other deductions.

Your Social Security check is your gross benefit less deductions.

If you start Social Security before or after your FRA, you get a smaller or larger gross benefit.

Hedgmatic uses your PIA and start age to compute your gross benefit. If you don’t know your PIA, Hedgematic can use your start age and associated gross benefit to compute your PIA.

You can see these numbers by creating a Social Security account at ssa.gov/myaccount. You also may get a yearly mailed Social Security Statement that contains the same information. Depending on your age, and whether or not you are already taking Social Security, different figures are provided:

If you are already taking social security, you see gross benefit, but no PIA.

If you are not yet taking Social Security,

And you are younger than your FRA, you see your PIA, aka “estimated benefit at full retirement age.

If you have passed FRA, you see the gross benefit if you retire today, from which the PIA can be computed.

Filling in the Primary Insurance Amount

I don’t have my Social Security Statement

Hedgematic will create a rough estimated PIA based on your current salary.

Drop the helper in the “Primary Insurance Amount” field.

Select “Salary”.

Enter yearly salary

Helper closes, estimated PIA is shown.

I’m Already Taking Social Security

Drop the helper in the “Primary Insurance Amount” field.

Select “Benefit”.

Enter gross benefit (your check before deductions). This is also available on your SSA account, or your yearly mailed COLA letter.

Helper closes, estimated PIA is shown.

I’m Younger Than 62

You don’t see the Benefit helper. It only works if you are old enough for Social Security. Use the salary estimator, or,

Your PIA is called out on your Social Security Statement. Enter PIA in the “Primary Insurance Amount” field.

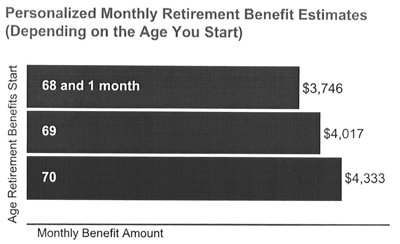

I’m Older Than 62 and not taking Social Security

If you are younger than your full retirement age, your statement provides your PIA. You can go ahead and enter it.

Once you are past full retirement age, your statement no longer tells you your PIA. It does, however, tell you your gross benefit if you retire at your current age.

Drop the helper in the “Primary Insurance Amount” field.

Select “Benefit”.

Enter your Personalized Monthly Retirement Benefit Estimate for your current age. Below, the number is $3746.

Helper closes, estimated PIA is shown.

Setting the Social Security Start Age

Start Ages for you and your spouse are initially set to your FRAs.

Drag the slider to try different start ages.

After changes are made, updated social security benefits are displayed and totaled. Numbers are in today’s dollars. Your actual check will increase with inflation every year.

Important: Your social security start age need have no relationship to the day you stop working. Depending on your assets and expenses, you can often retire well before your first social security check.

5 - Your Expenses

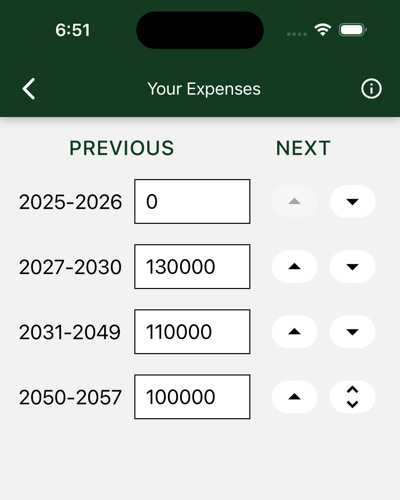

Enter after-tax, current-dollar income needs for each remaining year of your life

Hedgematic allows you to specify income requirements for each individual year of retirement. These figures should be entered in today’s dollars.

Values should be required actual after-tax take-home pay. Hedgematic draws will include estimated taxes in addition to these numbers. And you won’t be making retirement contributions either.

If you need the same amount every year, starting today, just type it in and move on. Hedgematic will tell you when your retirement can start.

If you anticipate different income requirements for upcoming phases of your life, set up multiple intervals and assign needed income to each,

using the buttons at the end of each row to:

Split the last year off into its own new row.

Move the last year of an interval down into the next row.

Move the first year of an interval up into the previous row.

Remove a one-year interval, by combining it with the previous row.

For example:

Our illustrated couple are ages 60 and 62. They wonder if they can retire in two years. They put zero expenses in the first two years.

They have a mortgage that will be paid off in 2030. They split off a second row, and enter enough to cover their mortgage and expenses.

The third row covers their active retirement after the mortgage is paid.

As they approach their eighties, they figure they’ll stay closer to home.

Hedgematic results will include the size of the estate resulting from the expenses you describe here.

6 - Your Balances

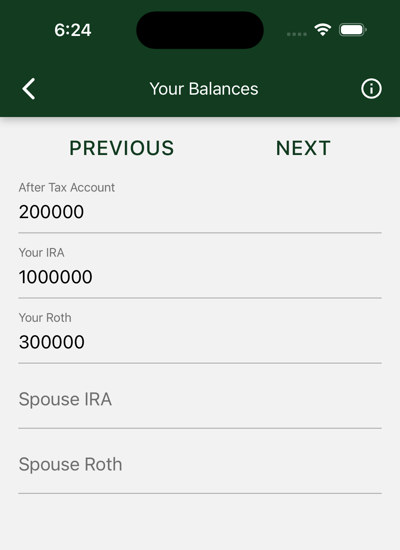

Enter account balances by type of account

List your accounts and their balances. If you have multiple accounts in the following categories, aggregate their balances and enter the total in the appropriate category.

After Tax is the balance of your savings that are not deposited in retirement accounts. Include accounts for you and your spouse.

For this and other accounts, leave the entry zero if no balance or no account.

Your IRA is the account balance of your IRA or 401K.

Spouse’s IRA is your spouse’s IRA or 401K balance.

Your Roth is your Roth or equivalent account balance. Hedgematic will schedule rollovers from your IRA as part of tax computation. There are some rules about transactions

in a new Roth account, so go ahead and get one, even if you have no deposits to make yet.

Spouse’s Roth is your spouse’s Roth balance.

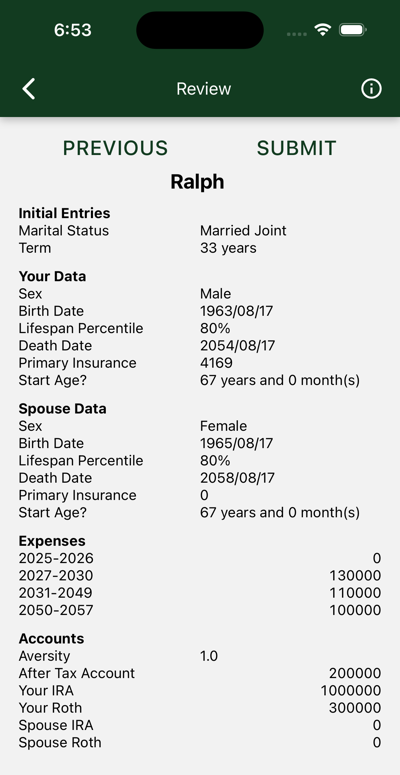

7 - Review

Review and submit your new profile

Review your new profile before pressing SUBMIT to save it.

You may use the PREVIOUS button to go back and fix any errors. (Warning: The back arrow at the top of the page will discard your efforts.)

You will not be able to edit this profile after you submit it. This is so you can compare results over time with the same data.

You can always delete this profile and make another, or clone this profile and make edits in the new profile.