Your after-tax, IRA, and Roth accounts each contain a mix of the following:

S&P ETF

TIPS Inflation Protected Bonds

Cash

When you are ready to commit to a particular portfolio computation, you find your shopping list for year 0 under each account, with a page for each asset type.

1 - S&P

S&P ETF

The S&P 500 is the oldest, most studied index of stock market performance. Hedgematic uses an S&P ETF to capture stock market income and gains. Your brokerage account and any retirement accounts each may have S&P holdings.

Hedgematic tracks S&P holdings in “S&P units”. Each unit is valued at the current S&P average. Your ETF will be priced differently. When you are directed to buy or sell so many units, multiply by the current S&P and divide by the current ETF to get the number of ETF shares to transact.

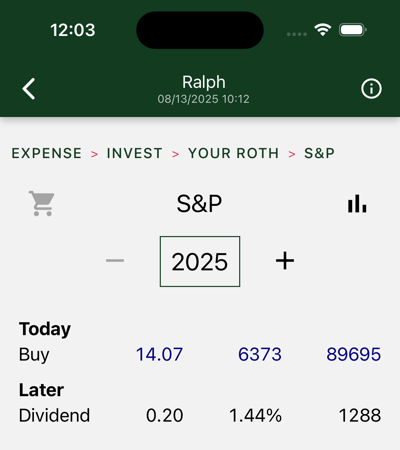

On day 0, inflation adjusted values and actual dollars are the same. In the first year, as displayed here, you have deployed all Roth assets to S&P.

Following the initial purchase, you are not directed to make any additional purchases, with the exception of reinvested dividends. (there are also in-kind rollovers). In effect, your S&P assets are split into individual tranches, each targeted at a particular year and “held to maturity.”

Hedgematic specifies S&P unit withdrawals for each year. You could just uninstall the app and follow the plan, withdrawing your yearly sums. More likely, you will look to rebalance each year.

The dollar figures shown in future years are estimates denominated in today’s dollars, so you should not expect them to match your future sale proceeds. Your proceeds, if you do back out future inflation, may come out higher or lower than the today’s dollar figures shown, which are modeled estimates. Navigate to the Lessons page to learn how this model is constructed and employed.

There is a chance that these proceeds may not meet your specified after-inflation expenses. You indicated your tolerance for this outcome with the risk aversity you included when you created your profile. But there will be a payday every year. Barring national catastrophe, you will not run out of money.

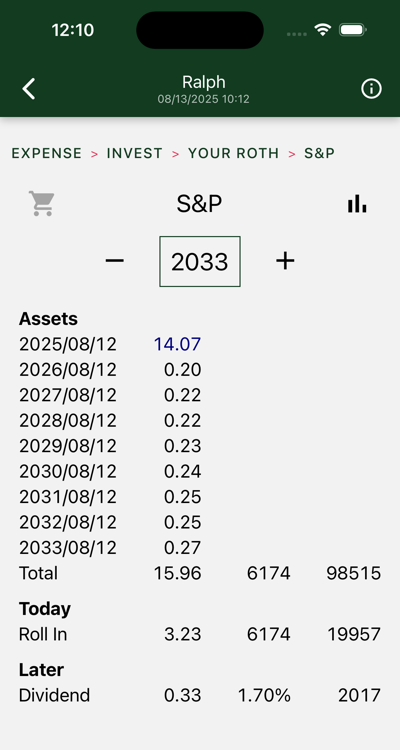

Above is an out-year display.

At the top of the screen, you see you are holding multiple lots of S&P. At the top is your original 14.07 S&Ps. Following you see reinvested dividends for nine years.

In 2033, you are instructed to roll 3.23 S&Ps from your IRA to this Roth.

In later years, you are instructed to sell part or all of particular tranches. Sale proceeds wind up in cash where they are drawn to support your year’s expenses.

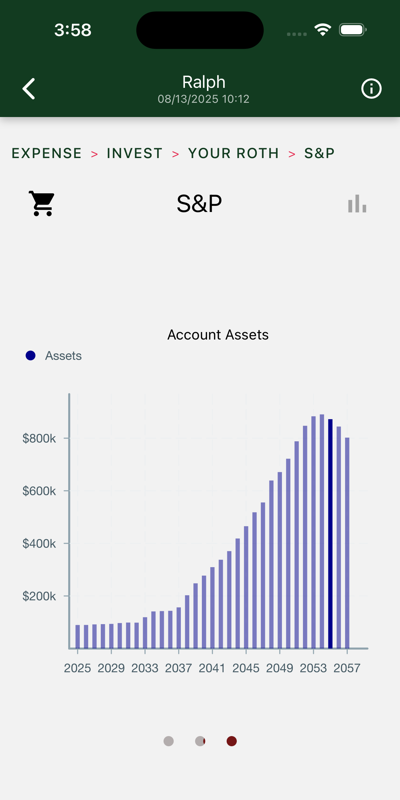

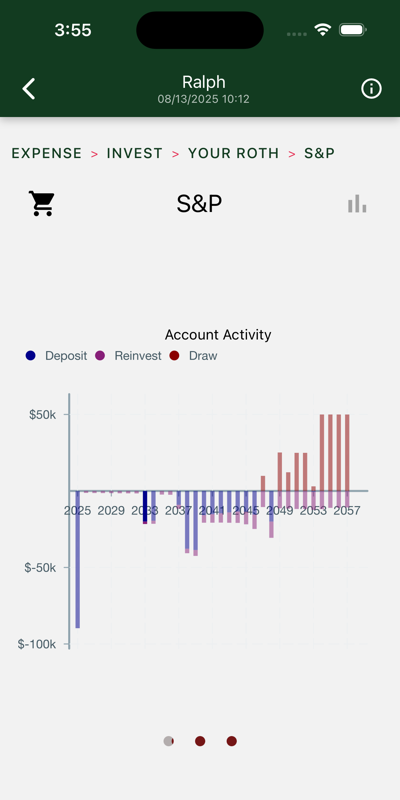

Charts

Three charts are shown. Swipe to view each in turn.

Account Assets

Yearly total account balances.

Account Activity

Withdrawals are on top. Initial purchases, reinvestments, and roll-ins are on the bottom.

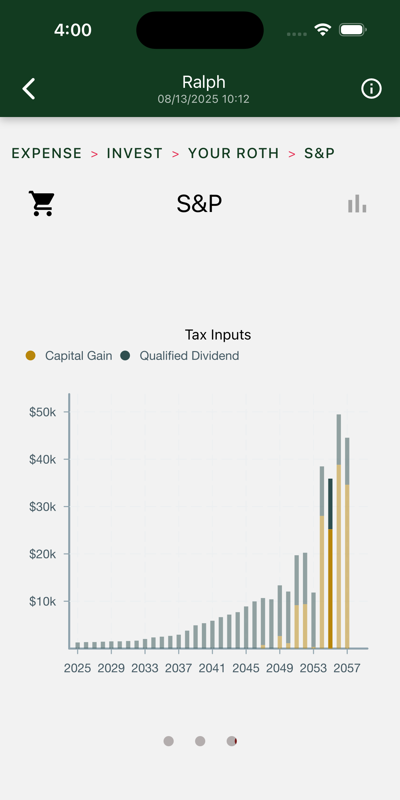

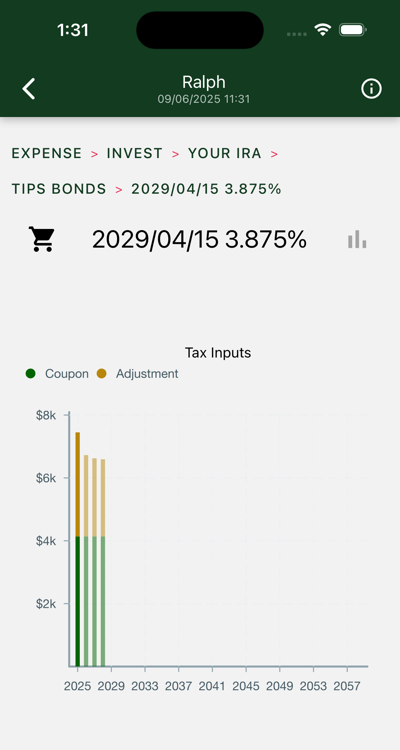

Tax Inputs

If we are in an after-tax account, these figures show up on your tax return. Otherwise, they are tax-free accumulations.

2 - TIPS Bonds

TIPS Inflation Protected Bonds

Hedgematic uses TIPS to to hold the inflation/market risk protected portion of your portfolio.

Bonds are purchased on day zero and held to maturity. We are not concerned about intervening volatility, as we are just purchasing a known current dollar sum as of the maturity date. Bond funds that mix maturity dates take on unnecessary market risk.

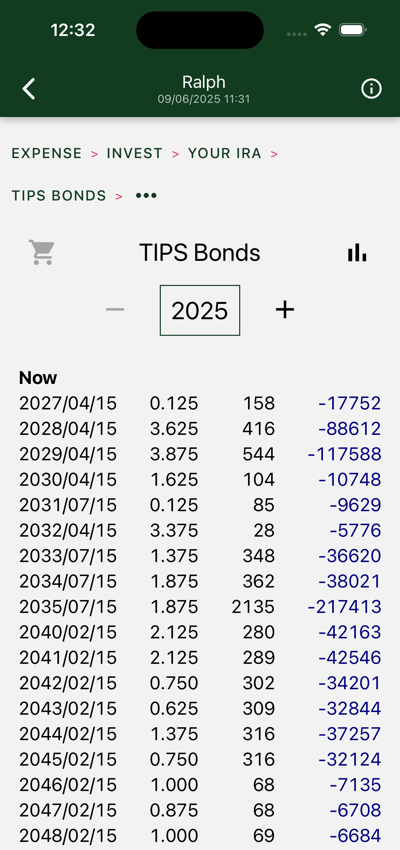

Displayed above is your day zero TIPS shopping list for your IRA account. You see a ladder of bonds,

each of which are redeemed in separate years to give you the guaranteed portion of your yearly expenses. Note that as the term increases, the values decrease. In the out years we can rely more on the typically more profitable S&P to provide more income.

Your broker will list these bonds with treasury bills. The maturity date and coupon yield (in column 2) is used to identify the specific bond.

When issued, these bonds are denominated at $100 “par” value. The third column tells you how many individual bonds you will buy. Many brokers deal only in $1000/ten bond trades. If that is the case, divide the quantities by ten and enter the rounded count in your order.

Since they were issued, their principal value has been contiuously updated for inflation, so you no longer see 158 bonds worth $15800. Your purchase price reflects the additional coupon and redemption value of the bond. This multiplier is called the factor, and is reported along with other bond info.

Bonds will pay coupons twice a year. In after-tax accounts, coupons and an inflation adjustment are reported as income.

Bond income and redemptions are drawn from the account at the end of the year and applied to next year’s expenses.

Figures shown in following years are denominated in today’s dollars, and can be relied on with one exception; the inflation adjustment shown is only an estimate and has an effect only in after-tax accounts.

Drill down to see more information on individual bonds.

Charts

Three charts are shown. Swipe to view each in turn.

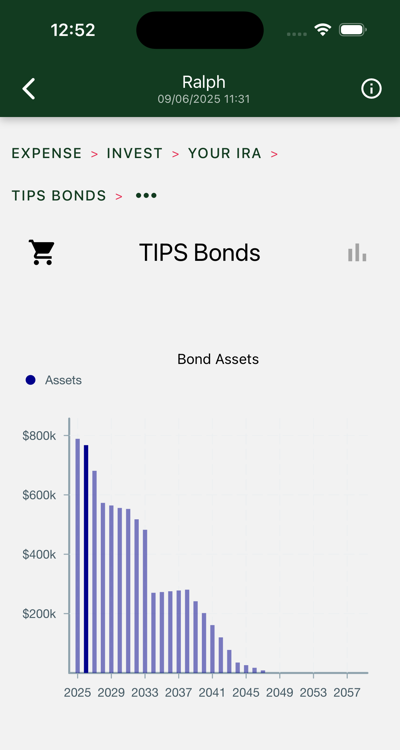

Bond Assets

Total bond value decreases as earlier maturities are redeemed.

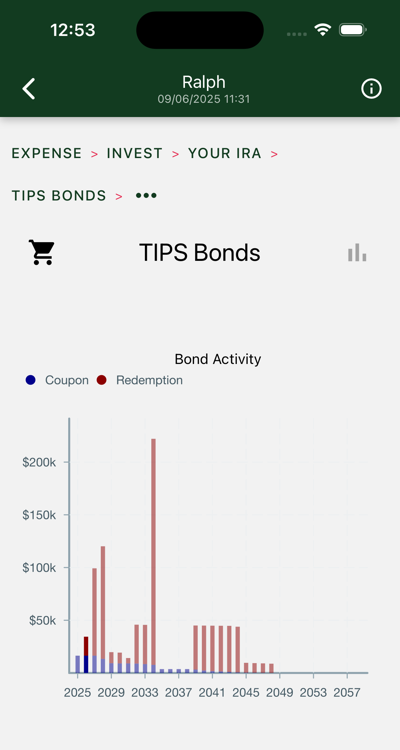

Bond Activity

Tall bars are redemptions. Tiny bars are coupons.

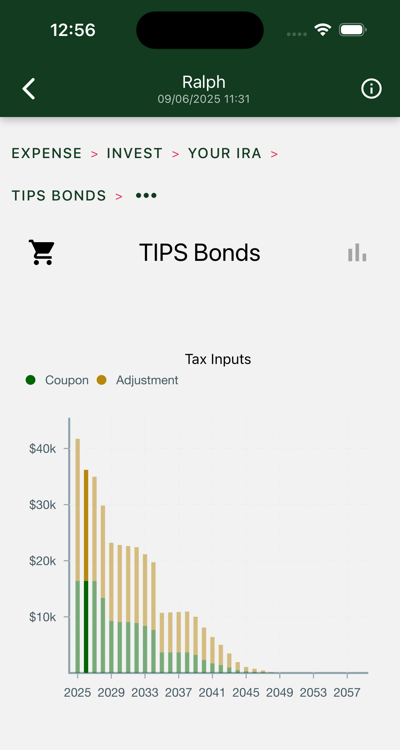

Tax Inputs

If we are in an after-tax account, these figures show up on your tax return. Otherwise, they document tax-free accumulations.

2.1 - TIPS Bond

Individual TIPS Inflation Protected Bonds

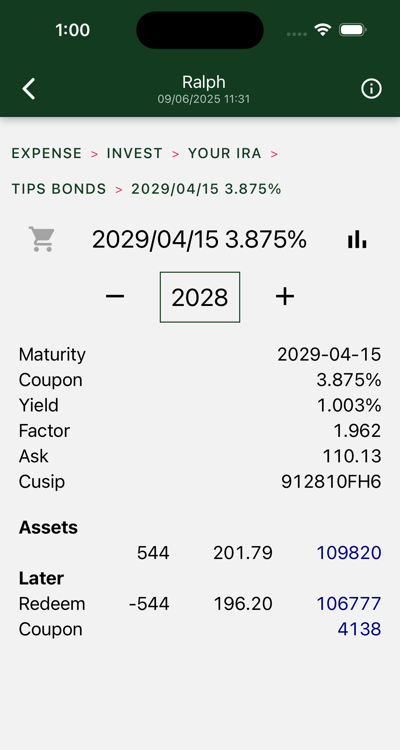

The information at the top of the page is commonly available when shopping for bonds.

Maturity is the date you get your redemption and last coupon. The redemption amount is computed by multiplying the factor and the number of bonds.

Coupon is paid twice a year. The coupon value is computed by multiplying the coupon rate and the factor and dividing by two. 3.875 * 1.962 / 2 = $3.80 for each bond, twice a year. 544 * $380 * 2 = the $4138 coupon value at the bottom of the page.

Yield is the real yield, in constant dollars. Your bonds will earn both real yield and inflation adjustments.

Factor tells you how much inflation has been added to this bond already. Here, the 1.962 tells you the bond, initially sold for $100, will be redeemed for almost $200 in current dollars, thanks to the power of compound inflation.

The ask is provided you as if the bond was still $100. Multiply ask and factor to get what you will pay for this bond. In this case, it cost $216.07.

The Cusip is an id you can use to search for a particular bond issue.

At the Broker’s

Visit your broker’s Treasury Bonds page. Locate the TIPS bonds.

Each issued bond has a maturity date and a coupon rate. Find the bond that matches the first two columns.

Buy the quantity shown in the third column. This is tricky. The amount you order is not the amount you pay.

These bonds have a “par value” of $100. If you want 158 bonds, you order 158 times $100 or $15800 (depending on broker, likely rounded to the nearest thousand).

The amount you pay, estimated in the fourth column, doesn’t match the order amount, and doesn’t match the figure in the fourth column. Your job is to turn the par value knob, and check whether the displayed cost amount is close.

The actual price of the bond is computed as the Factor times the Ask.

The Factor accounts for the inflation adjustment applied since the bond was issued.

The Ask responds to the Yield, and varies continuously throughout a session.

The amount you pay also includes adjustments to compensate the previous owner for their share of the next coupon.

Your broker will likely offer a ladder builder, where you can enter all the bonds you want first, then buy them in a single transaction.

Charts

Three charts are shown. Swipe to view each in turn.

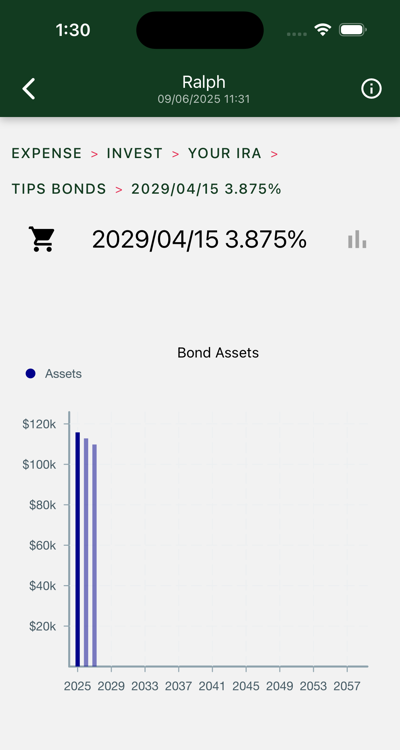

Bond Assets

Present value of bond declines as coupons are paid out.

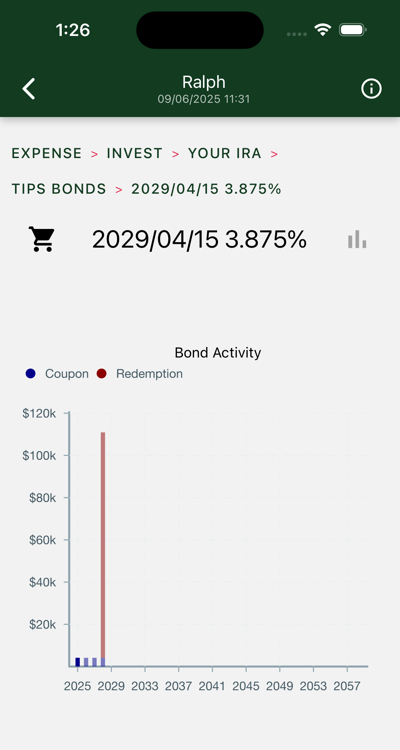

Bond Activity

See small coupons followed by big redemption.

Tax Inputs

The coupons are in today’s dollars. Your adjustments will vary. If the bond is held in a broker account you will have to pay taxes on both coupons and adjustments. These adjustments are estimates from yield curve data of future inflation rates.